Hidden Liabilities Complicate Pledge to Curb Overcapacity

Boya Wang

Executive Summary:

A significant share of local government borrowing is tied to renewable energy investments, supported by subsidized land, preferential financing, and special-purpose bonds.

Efforts to restructure local government debt, including maturity extension and debt for equity conversion, will ease near-term repayment pressures; but it could also perpetuate state subsidies and industrial overcapacity.

Overcapacity in renewable industries has intensified trade tensions, with Western governments raising concerns over subsidies and market distortions.

Amid rising pressure to rein in local government debt, in early November the Ministry of Finance established a new Debt Management Department (债务管理司). The new organ is tasked with formulating and implementing domestic government debt management systems and policies for central and local governments, preparing plans for the outstanding balance limits of national bonds and local government bonds, and undertaking management tasks related to the issuance and redemption of domestic government debt. It will also manage foreign government debt and strengthen the monitoring and supervision of government debt to prevent and mitigate hidden debt risks (Ministry of Finance [MOF], November 3, 2025).

The creation of the new department reflects a broader policy shift away from loosely scrutinized fiscal expansion aimed at boosting GDP growth and toward tighter controls to curb and reduce local government indebtedness. The move was signaled at a press conference in September, when Finance Minister Lan Fo’an (蓝佛安) said that his ministry’s focus over the next five years would include enforcing stricter limits on local government borrowing to ensure funds are used efficiently and remain repayable, strengthening life-cycle oversight of special-purpose bonds from issuance to repayment, integrating the management of implicit and statutory debt, and building a unified long-term regulatory framework (Securities Times, November 3, 2025).

On December 27, 2025, Chen Daofu (陈道富), deputy director of the Financial Research Institute at the State Council’s Development Research Center, underscored the growing policy focus on “revitalizing existing [state] assets” (盘活存量) as a key measure to address the sheer scale of local government debt (21st Century Business Herald, December 29, 2025). The statement echoes recent central policy documents—including the 2024 and 2025 central economic work conferences and the communiqué from the Fourth Plenary Session of the 20th Central Committee—where “state asset revitalization” (盘活国有资产) has been elevated to a core strategy for improving resource allocation efficiency. Those meetings led to measures targeting underused public and quasi-public assets across municipal infrastructure, industrial and business parks, and project start-up funding, and implicitly guaranteed local government loans (Xinhua, December 12, 2024, October 23, 2025, December 11, 2025).

Government Debt Bound Up in Underperforming Renewables Investments

No official figures have been released, but media reports suggest that a significant share of local government debt is linked to, or directly invested in, the renewable energy. The “Guiding Opinions of the National Energy Administration on Promoting the Integrated Development of New Energy” (关于促进新能源集成融合发展的指导意见) call for streamlining approval, grid connection, and licensing procedures for integrated new energy projects, encouraging one-stop administrative services. It also promotes multi-stakeholder collaboration between local governments and industry and proposes financial support through local government special-purpose bonds for eligible projects (National Energy Agency, October 31, 2025).

In the People’s Republic of China (PRC), extensive state support for renewable energy-related industries has become an increasingly contentious issue in trade relations with advanced economies. Large-scale subsidization—including low-cost loans and project start-up funding provided by local authorities—has enabled Chinese renewable energy companies, particularly suppliers of technologies and key components for electric vehicle (EV) batteries, solar power, and wind energy, to rapidly expand capacity, drive down global prices, and consolidate market share. This has raised concerns in the United States and the European Union about industrial hollowing-out and the erosion of strategic autonomy in clean technologies.

One U.S. response has been to threaten higher tariffs on solar products imported from Southeast Asia. These measures are aimed at countering the alleged circumvention of trade remedies by Chinese firms following sustained complaints from domestic manufacturers regarding injury from low-priced, subsidized imports. But the implementation of enforcement mechanisms may be difficult to achieve in practice (China Trade Monitor, October 27, 2025). The European Commission, meanwhile, launched an investigation in 2024 into wind farm developments across five EU countries, reflecting growing concern that Chinese turbine producers supported by state subsidies could undercut European competitors (European Commission, April 8, 2024, January 8). In February 2026, it opened an additional investigation into the PRC wind turbine manufacturer Goldwind Science & Technology on similar grounds (European Commission, February 3).

Beijing has gradually scaled back direct state subsidies for renewable energy in recent years, driven not only by external pressures but also by mounting fiscal strains at the local level and persistent “overcapacity” (产能过剩) concerns (China Brief, November 1, 2024). As renewable technologies have become increasingly cost-competitive, both central and local authorities have shifted away from generous feed-in tariffs and upfront subsidies toward more market-based mechanisms, including competitive bidding, grid-parity policies, and green certificate trading. This transition aims to reduce fiscal burdens, curb excessive investment and capacity expansion, and mitigate international accusations of trade-distorting state support, while still maintaining momentum toward the country’s “dual carbon” (双碳) targets of peaking carbon emissions by 2030 (碳达峰) and achieving carbon neutrality by 2060 (碳中和) (Xinhua, September 22, 2020, November 4, 2025).

The proliferation of the PRC’s renewable energy industries has been largely policy-driven. In this way, the sector has followed a similar course to those historically seen in other industrializing countries, characterized by strong state intervention and targeted support. Its prioritization has been signaled from the very top, with President Xi Jinping announcing the “dual carbon” goals at the United Nations General Assembly in September 2020. These targets were subsequently incorporated into the draft of the 14th Five-Year Plan (2021–2025), which was enacted in March 2021 (CCP Member’s Net, March 13, 2021). This economic blueprint embedded the dual carbon targets as a core component of the PRC’s national development strategy, and had a strong emphasis on energy system transformation and the expansion of renewable energy capacity.

In response to central economic directives, local governments have launched a number of administrative and fiscal support policies, including the disposal of land at preferential or below-market prices (低价出让土地), fiscal subsidies (财政补贴), and tax deductions (税收减免) (Peking University Guanghua School of Management, August 2, 2022; Pingtan Tax Society, November 24, 2025).

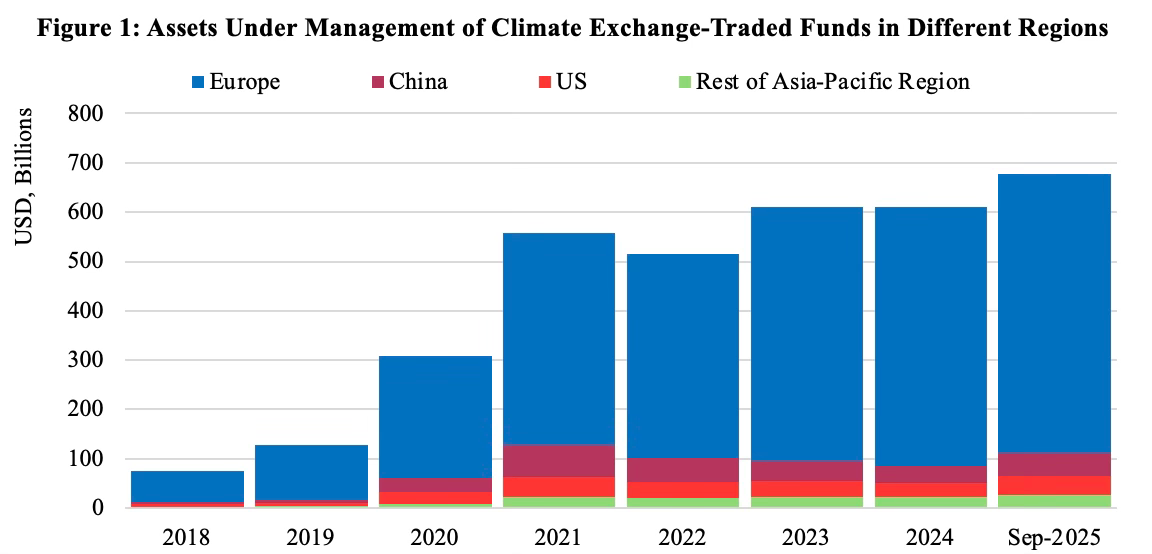

Alongside the rapid growth of renewable energy projects across the country, the “dual carbon” goals have emerged as a key theme for domestic equity market investments. Figure 1 shows that the total assets of Chinese exchange-traded funds (ETFs) with a focus on decarbonization and/or renewable energy generation overtook those of their U.S. peers from 2020. By the third quarter of 2025, assets invested in Chinese funds reached nearly $46 billion, compared with $39 billion in the United States and $27 billion in other economies in the Asia–Pacific region. Unlike other markets, though, investments in the PRC are largely driven by speculative retail investors.

Figure 1: Assets Under Management of Climate Exchange-Traded Funds in Different Regions

The PRC’s interventionist approach distorts market signals by encouraging excessive and redundant investment. The renewables sector is consequently experiencing mounting overcapacity and escalating price wars, ultimately leading to “involution” (内卷), whereby firms continue to expand output in order to secure subsidies or preserve market share without making corresponding improvements in efficiency or innovation. Industry-wide profits have declined persistently as a result, and the return performance of popular investee companies has been disappointing.

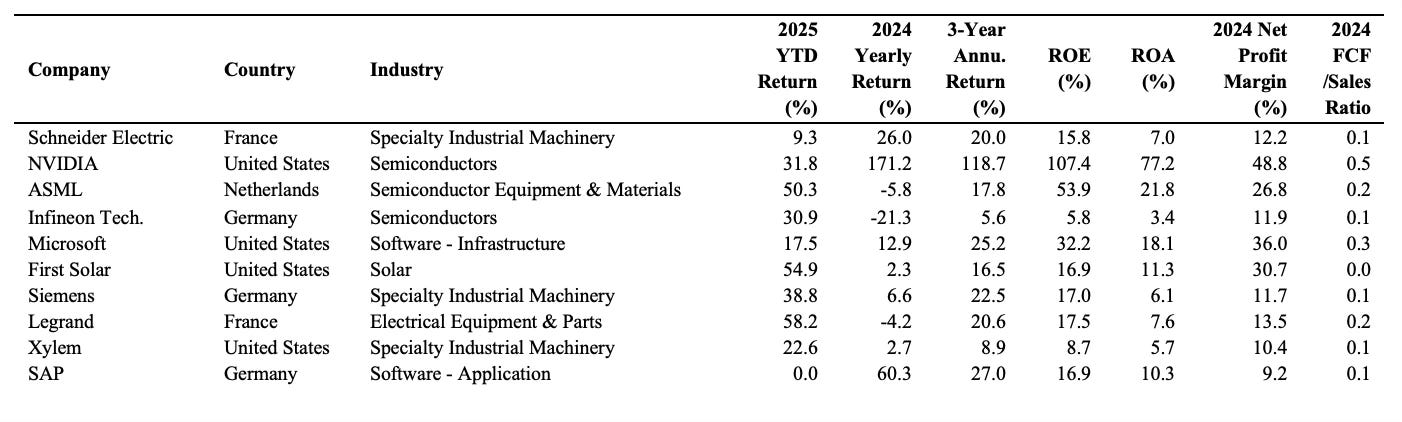

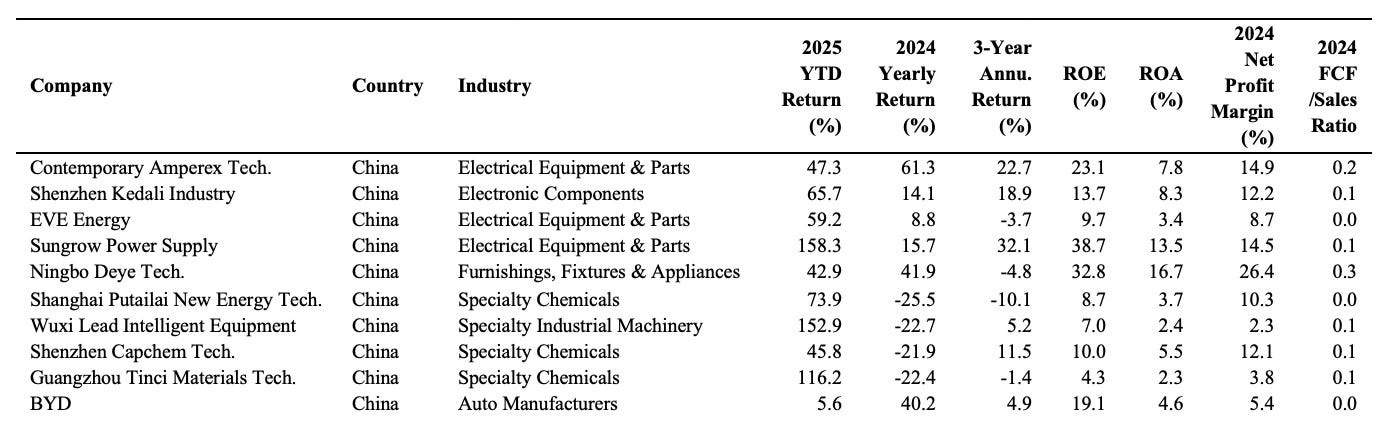

This is partly why the most commonly held stocks in Chinese ETFs featuring decarbonization and renewable energy mandates tend to underperform their Western peers in both short- and mid-term horizons. Despite a notable uptick in year-to-date (YTD) returns in 2025, largely driven by a small number of outliers, the three-year annualized return of the most commonly held stocks in Chinese climate funds averaged 7.5 percent, compared to 28.3 percent for their European counterparts. The average return on equity (ROE) and return on assets (ROA), at 16.7 percent and 6.8 percent, also lag Europe’s 29.2 percent and 16.9 percent, respectively, while the 2024 free cash flow-to-sales ratio (FCF/sales) was roughly half that of European firms (see Figure 2).

Figure 2a: Top 10 Common Holdings by European Climate Funds

Figure 2b: Top 10 Common Holdings by Chinese Climate Funds

Policy Shifts Driven by Debt Restructuring Priorities

The rollback of state support to industry intersects uneasily with ongoing local government debt restructuring and the weakening of land-based fiscal revenues. As land sales—traditionally a major source of local government finance—have slowed amid the property sector downturn, local governments face intensified pressure to stabilize revenues, maintain employment, and sustain growth while simultaneously containing debt risks. These factors are increasingly central to assessing local bureaucrats’ careers.

At the 17th meeting of the Standing Committee of the 14th National People’s Congress (NPC) on September 10, 2025, Lan Fo’an reported that government debt totaled Renminbi (RMB) 92.6tn ($13tn) in 2024, comprising RMB 34.6tn ($4.97tn) in central government debt, RMB 47.5tn ($6.82tn) in statutory local government debt, and an estimated 10.5tn ($1.51tn) in off-budget or hidden local government liabilities (隐性债务), with the government debt-to-GDP ratio standing at 68.7 percent at year-end (SCIO, September 13, 2025).

The estimated $1.51tn in off-budget or hidden liabilities is likely to understate the true scale of opaque local government financial obligations, which are primarily funneled through numerous local government financing vehicles (LGFVs). LGFVs mostly operate with substantial accounting opacity, as much of their debt remains off-balance-sheet and unconsolidated from official public finances, complicating accurate assessments of total liabilities. Delayed disclosures exacerbate these issues. Audits conducted by the National Audit Office (NAO) revealed previously unreported LGFV defaults and exposures. Accumulated during the 2008 economic stimulus, which at the time was a landmark policy response to the global financial crisis, these liabilities have belatedly surfaced only after financial stress forced acknowledgments (NAO, December 22, 2025).

Independent estimates place LGFV debt at over RMB 60tn ($8.62tn) by the end of 2024, roughly 45–50 percent of GDP—far above the figure released by the Ministry of Finance. Other analyses put it even higher, at up to RMB 78tn ($11.2tn). The International Monetary Fund (IMF) has revised the off-budget liabilities to include debts accumulated through LGFVs, government-guided funds, and special construction funds, yielding an augmented general government debt ratio of around 124 percent for 2024 (IMF, April 30, 2025; Kunath, 2025). [1]

Local city commercial banks are the largest creditors of LGFVs, funding local government infrastructure through loans and bond purchases, including debt swaps. Leaving aside state asset stripping and various corrupt practices, nearly 30 percent of total bank loans are tied to the property sector, where the ongoing downturn erodes collateral values and repayment capacity. The interconnectedness of this system risks a negative feedback loop: deepening property busts could trigger defaults of hidden local government liabilities, straining bank balance sheets and prompting systemic liquidity squeezes given banks’ role in absorbing nearly all LGFV-related financial risks.

Beyond the potential risks of bank contagion and currency depreciation, rising fiscal pressures undermine local governments’ capacity to deliver essential public services, including social safety nets for a rapidly aging population, particularly in the context of falling tax revenues. These spillover effects pose a direct threat to social and political stability, a concern for both central and local policymakers, while also undermining the perceived legitimacy of the leadership.

In 2023, the PRC allowed an initial group of 12 heavily indebted provinces and municipalities, including Gansu, Liaoning, Jilin, Guizhou, Tianjin, and Chongqing, as well as the autonomous regions of Qinghai, Ningxia, and Inner Mongolia, to issue RMB 1.5tn ($220bn) special-purpose bonds to refinance hidden local government debts. This measure aimed to transfer off-balance-sheet obligations onto official balance sheets and alleviate immediate liquidity pressures, and marked an early step in formalizing opaque liabilities accumulated through LGFVs (Caixin, March 6, 2024).

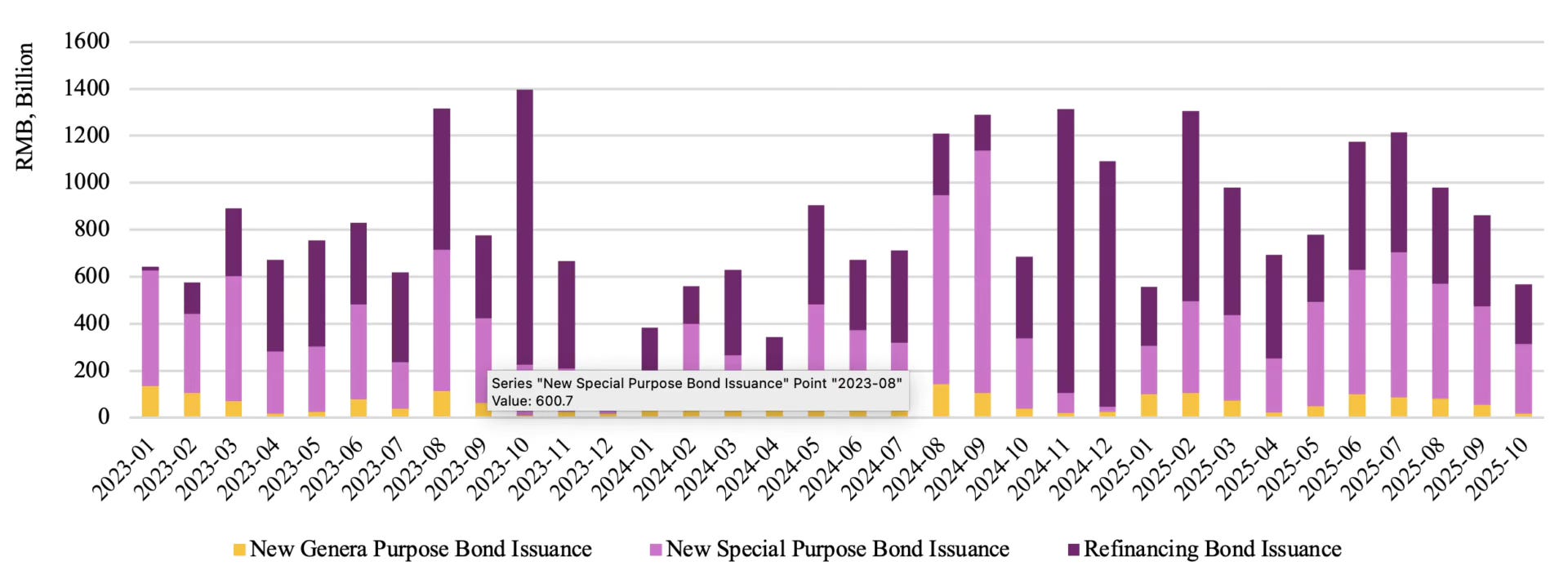

A more expansive debt resolution (化债) measure followed in November 2024, when the NPC approved an RMB 10tn ($1.44tn) debt package over five years to address hidden local government debt that had totaled RMB 14.3tn ($2.05tn) at the end of 2023. This included, starting in 2024, the allocation of RMB 800bn ($115bn) per year from newly issued local government special-purpose bonds to supplement government fund resources specifically for debt repayment, enabling a cumulative replacement of up to RMB 4tn ($575bn) in hidden debt. The package, approved by the NPC Standing Committee, also included an additional RMB 6tn ($862bn) in local government special bonds (MOF, November 9, 2024). The core of the resolution plan was referred to as “trading space for time” (空间换时间), and relied on the swap of high-interest, short-term debts for lower-interest, longer-maturity official bonds to ease near-term repayment pressure. This measure is projected to save RMB 6bn ($862 million) in interest payments over five years. As illustrated in Figure 3 below, debt issued by the government for refinancing purposes has represented the largest share of new government debt issuance since mid-2023.

Figure 3: Distribution of Government Bonds Issued Between January 2023 and October 2025

Debt swaps alone will not eliminate repayment risks, as LGFVs generally lack sufficient self-sustaining cash flow-generating capacity, an issue that is becoming increasingly concerning for both local and central policymakers. Against this backdrop, authorities encourage LGFVs to be restructured into commercially viable operators of municipal public services and local industrial and science parks, facilitating the conversion of existing debt claims into equity stakes. This is critical, as the actual size of hidden local government debt remains largely uncertain.

Alongside debt-to-equity conversions, industrial parks and related infrastructure remain the largest recipients of newly issued debt. According to statistics from the Ministry of Finance, in the first three quarters of 2025, local governments issued almost RMB 3.7tn ($540bn) in new special-purpose bonds for project construction, with allocations of approximately 28 percent to municipal and industrial park infrastructure, 18 percent to transportation, 14 percent to land reserves, 12 percent to affordable housing, 12 percent to social services (including healthcare, cultural tourism, and education), and 6 percent to agriculture, forestry, and water conservancy projects (Shanghai Securities News, October 11, 2025). Against this background, a large number of local industrial parks containing renewable energy-related assets are likely to remain in place at least in the short term, although their utilization and commercial competitiveness vary.

Conclusion

Renewable energy projects may continue to be promoted as quasi-fiscal instruments through preferential land allocation, implicit guarantees, and various start-up funding. Such practices risk perpetuating investment-driven expansion and excess capacity, while undermining market competition mechanisms needed to resolve overcapacity issues. At the same time, structural frictions in the PRC’s central–local fiscal relationship (particularly the slow progress of resolving the sheer scale of LGFV-related debts), rather than any adjustment in the government’s interventionist approach alone, are further compounding ongoing trade tensions.

This article originally appeared in China Brief. Check it out here!

Boya Wang is a Senior Analyst in Sustainable Investing Research at Morningstar Sustainalytics. He is also a Research Associate at the Centre for Business Research at Cambridge Judge Business School, where his research focuses on the role of local political and social institutions in shaping corporate governance practices and business risks in major emerging markets. Previously, he served as a Regional Economist at the Office of the United Nations High Commissioner for Human Rights. Prior to this, he was the Quantitative Research Lead for the Oxford Ownership Project at Oxford Saïd Business School.

Notes

[1] Kunath, Gero, 2025, “Debt-fuelled growth in China and local government indebtedness. The consequences of an unbalanced economic growth model,” IW-Report, Nr. 35, Köln.

Local government debt via LGFVs emerged as a response to strict borrowing constraints under the pre-2014 Budget Law (预算法), combined with fiscal decentralization and strong growth incentives. LGFVs allowed local governments to circumvent borrowing restrictions on local governments and to finance infrastructure and development projects off balance sheet, particularly following the 2008 stimulus. Although the 2014 revised Budget Law allowed local governments to issue on-budget bonds, aiming to replace LGFV borrowing with transparent debt, LGFVs have persisted, leaving a large stock of opaque liabilities backed by implicit government guarantees. LGFV debt servicing has historically relied heavily on local land sales and real estate activity. Land conveyance fees (土地转让费用) once accounted for 30–40 percent of total local fiscal revenue in many regions, providing crucial cash flow for both budgets and off-balance-sheet obligations. After the property market downturn post-2020, land sales fell sharply in both volume and price, eroding this primary revenue source. Cash flows supporting LGFV debt servicing and refinancing largely vanished, exposing structural repayment vulnerabilities and triggering widespread fiscal stress among local governments and their financing vehicles.

[2] International Monetary Fund. Asia and Pacific Dept “People’s Republic of China: Financial Sector Assessment Program-Financial System Stability Assessment-Press Release; Staff Report; and Statement by the Executive Director for the People’s Republic of China,” IMFStaff Country Reports 2025, 100 (2025).